Clean-Energy Trends 2006

At long last, the tipping point is nigh: For the first time in modern history, clean-energy technologies are becoming cost-competitive with their "dirtier" counterparts. While oil and natural gas prices remain stubbornly high and frustratingly volatile across the globe, and as nuclear and coal-based energy remain dogged by environmental and safety concerns, clean-energy prices continue their near-relentless downward march.

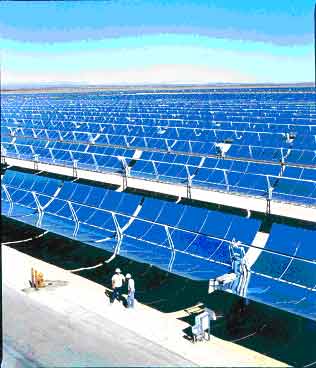

At long last, the tipping point is nigh: For the first time in modern history, clean-energy technologies are becoming cost-competitive with their "dirtier" counterparts. While oil and natural gas prices remain stubbornly high and frustratingly volatile across the globe, and as nuclear and coal-based energy remain dogged by environmental and safety concerns, clean-energy prices continue their near-relentless downward march.Consider wind power. In certain regions, it is now one of the least expensive and most easily deployed sources of new generating capacity. Or ethanol, which has gained favor for vehicle use in both in the U.S. and abroad. Or biodiesel, made from a wide range of animal and vegetable oils, whose price is within striking distance of petroleum-based diesel. Even solar, still relatively expensive without subsidies, competes favorably in some places and is often the cheapest choice for power in remote regions.

Suddenly, so-called "alternative" energy technologies are looking pretty mainstream.

The growth of clean-energy markets reflects its growing acceptance. Global wind and solar markets reached $11.8 billion and $11.2 billion in 2005 -- up 47% and 55%, respectively, from a year earlier. The market for biofuels hit $15.7 billion globally in 2005, up more than 15% from the previous year.

Multinationals like Archer Daniels Midland, BP, GE, Sharp, and Toyota are partly responsible for stoking these technologies' aggressive growth, leading the way with billion-dollar divisions dedicated to solar, wind power, ethanol, and hybrid electric vehicles, among other technologies. State and city governments throughout the U.S. are playing a key role, too, competing feverishly to become clean-energy hubs that attract economic development and jobs. The Silicon Valley venture firms that financed the Internet and wireless telecom revolutions -- among them Draper Fisher Jurvetson; Kleiner Perkins Caulfield & Byers; Mohr, Davidow Ventures; and VantagePoint Venture Partners -- have begun placing increasingly bigger bets on clean-energy.

Even America's Oilman, George W. Bush, seems to be warming to clean energy. In his 2006 State of the Union address, he declared what pretty much every other American already knew: the U.S. is "addicted to oil." Not an inconsequential statement for a Texan whose vice president once dismissed energy conservation as merely a "personal virtue." Bush proposed an initiative that calls for a 22% increase in clean-energy research and a goal of replacing at least 75% of U.S. Middle East oil imports by 2025 (though he offered no substantive funding to do these things).

Even without federal intervention, global clean-energy markets will flourish. According to Clean Edge research, biofuels (global manufacturing and wholesale pricing of ethanol and biodiesel) will grow from $15.7 billion in 2005 to $52.5 billion by 2015. Wind power (new installation capital costs) will expand from $11.8 billion in 2005 to $48.5 billion in 2015. Solar photovoltaics (including modules, system components, and installation) will grow from an $11.2 billion industry in 2005 to $51.1 billion by 2015. And the fuel cell and distributed hydrogen market will grow from $1.2 billion (primarily for research contracts and demonstration and test units) last year to $15.1 billion by 2015.

In total, we project these four clean-energy technologies, which equaled $40 billion in 2005, to grow fourfold to $167 billion within the coming decade.

It's not all smooth sailing, however: There remains turbulence in the clean-energy sector. The solar industry is experiencing growing problems, unable to gain access to enough silicon feedstock to keep pace with demand. It will continue to put pressure on upward pricing over the short term. Biofuels, while showing great promise, face obstacles, not the least of which is how to quickly ramp up widespread distribution channels. Growth of wind turbines, while currently expanding rapidly, could flag as well as short-term price increases due to high steel costs and shifting currency valuations. And mass adoption of fuel cells and hydrogen remain decades away.

We believe many such obstacles are surmountable through a combination of incremental and breakthrough technology developments, the continued scale-up of manufacturing, and smart investments by corporations, investors, and governments. As we've seen over the last five years since issuing our first report on clean technologies (Clean-Tech: Profits and Potential, April 2001), the market has considerable momentum and represents one of the fastest-growing technology sectors on the planet.

Solar Shines for Investors

It could be said that 2005 was the Year of the Sun. On both the private and public markets, solar outshined other energy technologies. VCs put more than $150 million into U.S.-based companies such as Advent Solar, Energy Innovations, Heliovolt, MiasolŽ, Nanosolar, and PowerLight in 2005 -- double the investments in 2004.

Solar's glow was even more evident in the public markets. The three largest technology IPOs of 2005 were for solar companies: Q-Cells, SunPower, and Suntech Power. Combined, they raised more than $800 million (on the Frankfurt, NASDAQ, and NYSE exchanges, respectively), and by the end of their first trading day, each had market capitalizations exceeding $1.5 billion.

Clean-tech stocks in general are doing well. A number of clean-energy stalwarts are trading at or near their 52-week highs. At the time of publication, Energy Conversion Devices (ENER), Evergreen Solar (ESLR), Itron (ITRI), and Spire Corp. (SPIR) were all trading at roughly double their year-ago levels. But stock prices for other clean technologies, including fuel cells and microturbines, showed less energy.

U.S.-based venture capital investments in energy technologies increased from $716 million in 2004 to $917 million in 2005. As a percent of total VC investments, energy tech increased from 3.3 percent in 2004 to 4.2 percent in 2005. Over the last six years, venture investments have more than quadrupled as a percent of total VC investments, increasing from under 1 percent of total venture investments in 1999 to last year's 4.2 percent.

Clean Energy State of Mind

In the United States, clean energy has become a politically unifying issue with wide support from those of every political stripe, from traditional liberals to current and former military brass. This bipartisanship has been particularly evident at the state level, where nearly twenty states now have renewable portfolio standards (RPS) that mandate a percentage (often up to 20-25 percent) of electricity coming from clean energy. States like California, Hawaii, New York, and Pennsylvania are embarking on aggressive -- and impressive -- clean-energy programs.

It's a trend we expect to continue as states view clean energy as an opportunity to address air pollution, public health problems, greenhouse gases, and grid congestion -- and a way for states to become known as centers for clean-technology development, with all the new jobs and businesses that can result.

Download the full report

posted by admin @ 2:50 PM

![]()

![]()

0 Comments:

Post a Comment

<< Home